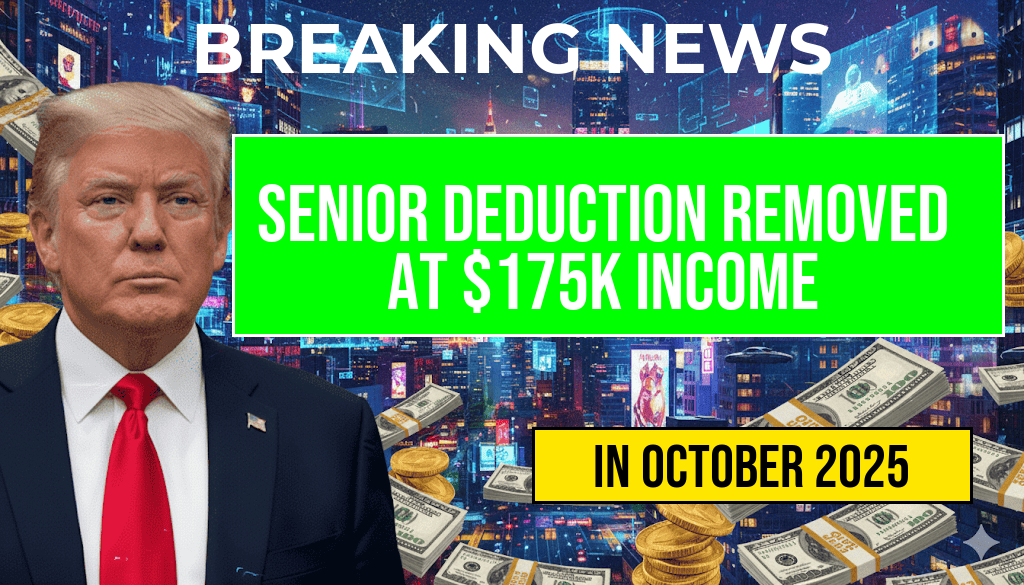

Effective this tax year, seniors earning an income of approximately $175,000 will no longer qualify for a $4,000 standard deduction. This change marks a significant shift in federal tax policy, impacting a demographic that often relies on fixed or retirement income. Previously, seniors with incomes below certain thresholds could benefit from this additional deduction, which aimed to offset expenses associated with aging. The elimination of the deduction at this income level reflects broader efforts to streamline tax brackets and reduce complexity, but it also raises questions about fairness and financial planning for retirees with higher incomes. Tax experts warn that affected seniors may see an increase in taxable income and, consequently, a rise in overall tax liability. The adjustment underscores the importance of careful income management and proactive tax planning for seniors approaching or surpassing the new threshold.

Understanding the Deduction Change

The decision to eliminate the $4,000 senior deduction at an income of $175,000 aligns with recent reforms aimed at simplifying tax codes and reducing disparities across income brackets. Historically, seniors with lower or moderate incomes have benefited from additional deductions designed to ease the financial burden associated with healthcare, housing, and other aging-related expenses. However, as income levels rise, the tax code has gradually phased out these benefits to ensure a more uniform tax treatment across different income groups.

Background and Policy Rationale

The deduction was introduced decades ago as part of broader efforts to support senior citizens, many of whom live on fixed incomes. Over time, adjustments were made to phase it out for higher earners, but the threshold remained relatively generous. Recent policy shifts, however, have aimed to reduce federal expenditures and simplify the tax code by eliminating certain deductions for individuals with incomes exceeding specified levels.

According to the Wikipedia entry on U.S. taxation, the federal government has periodically re-evaluated tax benefits to balance revenue needs with social support programs. The recent change specifically affects seniors, who often have limited options for increasing income and must adapt their financial planning accordingly.

Impact on Senior Taxpayers

| Income Level | Previous Deduction | Post-Change Deduction |

|---|---|---|

| $150,000 | $4,000 | $4,000 |

| $175,000 | $4,000 | Eliminated |

| $200,000 | Eliminated | Eliminated |

For seniors earning just below the new threshold, the loss of this deduction means a direct increase in taxable income by up to $4,000. This can result in higher federal tax bills, especially for those relying heavily on retirement savings and Social Security benefits. Financial advisors recommend reviewing current income streams and exploring strategies such as Roth conversions or tax-efficient withdrawal plans to mitigate the impact.

Broader Tax Policy Context

The elimination of the senior deduction at higher income levels is part of a broader trend to phase out various tax breaks that benefit specific groups. The aim is to create a more equitable tax system and improve revenue collection. Critics argue that this move disproportionately affects seniors who have limited options for increasing their taxable income without risking their financial stability.

According to Forbes, policymakers contend that the change encourages higher earners to contribute proportionally more to public finances, but opponents warn it could accelerate financial strain for retirees.

Next Steps for Affected Seniors

- Review Income Sources: Seniors should analyze all income streams, including pensions, Social Security, and investment earnings, to determine the precise impact of the deduction removal.

- Consult Tax Professionals: Engaging with qualified tax advisors can help identify strategies to offset increased liabilities, such as maximizing itemized deductions or utilizing tax credits.

- Adjust Financial Plans: Consider reevaluating withdrawal timings from retirement accounts or exploring tax-advantaged accounts to reduce taxable income.

Resources for Further Guidance

Frequently Asked Questions

What is the recent change to the senior deduction amount?

The Senior Deduction of Four Thousand Dollars has been eliminated for individuals with an income of One Hundred Seventy-Five Thousand dollars or more.

Who is affected by the elimination of the senior deduction?

Senior taxpayers with an income of $175,000 or higher are affected, as they will no longer be eligible for the $4,000 deduction.

When did the elimination of the senior deduction take effect?

The change took effect in the current tax year, impacting filings starting from that period onward.

How does this change impact seniors with high income?

Seniors with an income above $175,000 will see less tax relief through the deduction, potentially increasing their taxable income.

Are there any alternative deductions available for seniors with high income?

While the Senior Deduction has been eliminated at high income levels, seniors may still explore other tax credits and deductions available based on their individual circumstances.