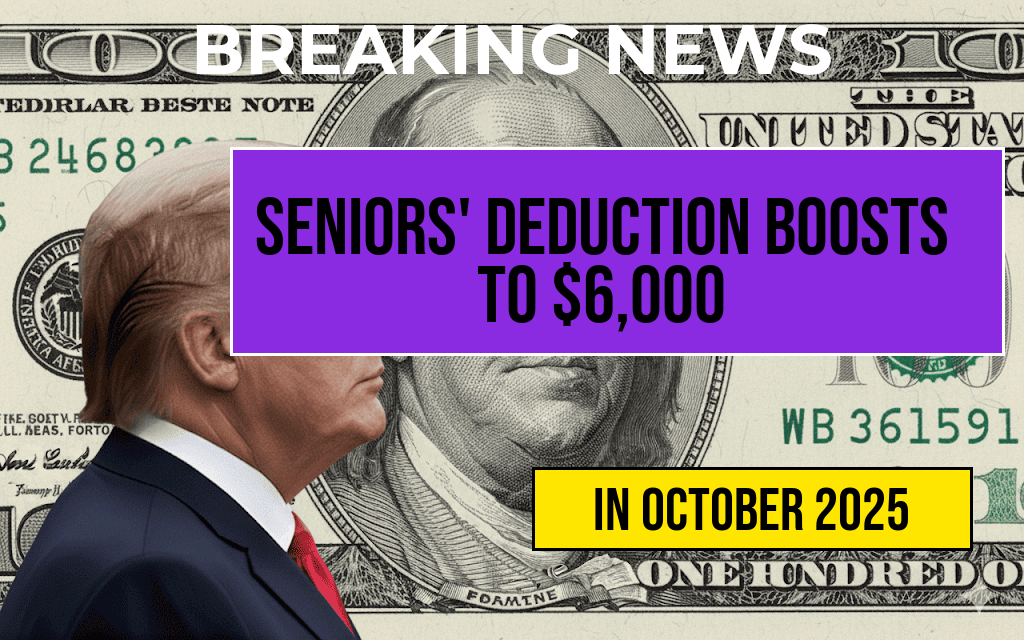

Beginning this tax year, seniors in the United States will benefit from an increased deduction limit, rising from $4,000 to $6,000. This adjustment aims to provide much-needed financial relief amid ongoing economic pressures and rising healthcare costs. The change, part of recent legislative updates, is intended to ease the tax burden for elderly taxpayers, especially those with substantial medical expenses or dependent care costs. The increased deduction applies primarily to itemized deductions related to unreimbursed medical expenses, dependent care, and certain other qualifying costs. Experts suggest that this change could significantly impact the tax planning strategies of seniors, allowing for more comprehensive deductions and potentially reducing overall taxable income. As the IRS begins implementing these updates, seniors are encouraged to review their financial situations and consult with tax professionals to maximize the benefits of the new deduction limit.

Understanding the New Deduction Limits for Seniors

Background on Deduction Changes

Prior to this adjustment, seniors could deduct up to $4,000 for qualified medical expenses and other eligible costs. The recent legislative change increases this cap to $6,000, aligning with inflation adjustments and the rising costs associated with healthcare and dependent care. The update reflects ongoing efforts by policymakers to address the financial challenges faced by older Americans, especially as healthcare needs become more complex with age.

Who Qualifies for the Increased Deduction?

- Seniors aged 65 and older

- Taxpayers with significant unreimbursed medical expenses

- Individuals supporting dependents or elderly relatives

While the increased deduction primarily benefits seniors, it also applies to taxpayers supporting elderly or disabled relatives, provided they meet the IRS criteria for dependents and expenses.

Implications for Tax Planning and Filing

Enhanced Medical Expense Deductions

The rise from $4,000 to $6,000 in deductible expenses enables seniors to claim larger deductions for unreimbursed medical costs. These include hospital visits, prescription medications, long-term care services, and certain insurance premiums. Taxpayers should maintain detailed records and receipts to substantiate their claims, especially as the IRS emphasizes documentation for larger deductions.

Impact on Dependent Care and Other Expenses

Beyond medical expenses, the increased deduction limit also applies to qualifying dependent care costs, which can include expenses related to adult dependents such as elderly parents or relatives requiring assistance. The higher threshold may allow many seniors to offset a larger portion of these costs against their taxable income.

Potential Benefits and Challenges

Financial Relief for Seniors

| Aspect | Previous Limit | New Limit |

|---|---|---|

| Medical and related expenses deduction | $4,000 | $6,000 |

| Eligible expenses cap for dependent care | $4,000 | $6,000 |

The increased limits could result in substantial tax savings for seniors with high medical bills or dependent care costs, potentially lowering their overall tax liability and freeing up resources for other essential expenses.

Challenges in Navigating New Regulations

While the higher deduction limits offer benefits, seniors and their tax advisors must stay vigilant to ensure compliance with IRS rules and documentation requirements. Additionally, the increased thresholds may not benefit all taxpayers equally, especially those with lower medical expenses or fewer qualifying costs.

Resources and Next Steps for Seniors

Seniors should review the IRS guidelines and consult with qualified tax professionals to determine how the new deduction limits impact their filings. For more information on itemized deductions and eligibility criteria, visit the IRS official site. Additionally, understanding broader tax credits and benefits available to seniors can help optimize overall tax strategies, as detailed on resources like Wikipedia’s page on Seniors in the United States.

Frequently Asked Questions

What is the new deduction amount available for seniors?

The new deduction amount for seniors has increased to $6,000, up from the previous $4,000.

Who qualifies as a senior for this increased deduction?

Seniors who meet the age requirement specified by the IRS, typically age 65 or older, are eligible for the increased deduction.

When did the increased deduction amount take effect?

The increase to the $6,000 deduction applies starting from the current tax year, reflecting recent tax law changes.

How does the increased deduction benefit senior taxpayers?

The increased deduction allows seniors to reduce their taxable income more significantly, potentially lowering their overall tax liability.

Are there any other tax benefits available to seniors besides the increased deduction?

Yes, seniors may also be eligible for additional tax credits and exemptions, which can further reduce their tax burden alongside the increased deduction amount.